Meteora is stirring the Solana group with a controversial proposal: to allocate 3% of the TGE fund to JUP stakers, not in common tokens however in Liquidity Position NFTs.

This novel method guarantees to bootstrap deep liquidity for MET from day one, but it raises questions on equity and focus danger. Will this be a savvy transfer to bridge the 2 communities, or will it ignite a protracted debate?

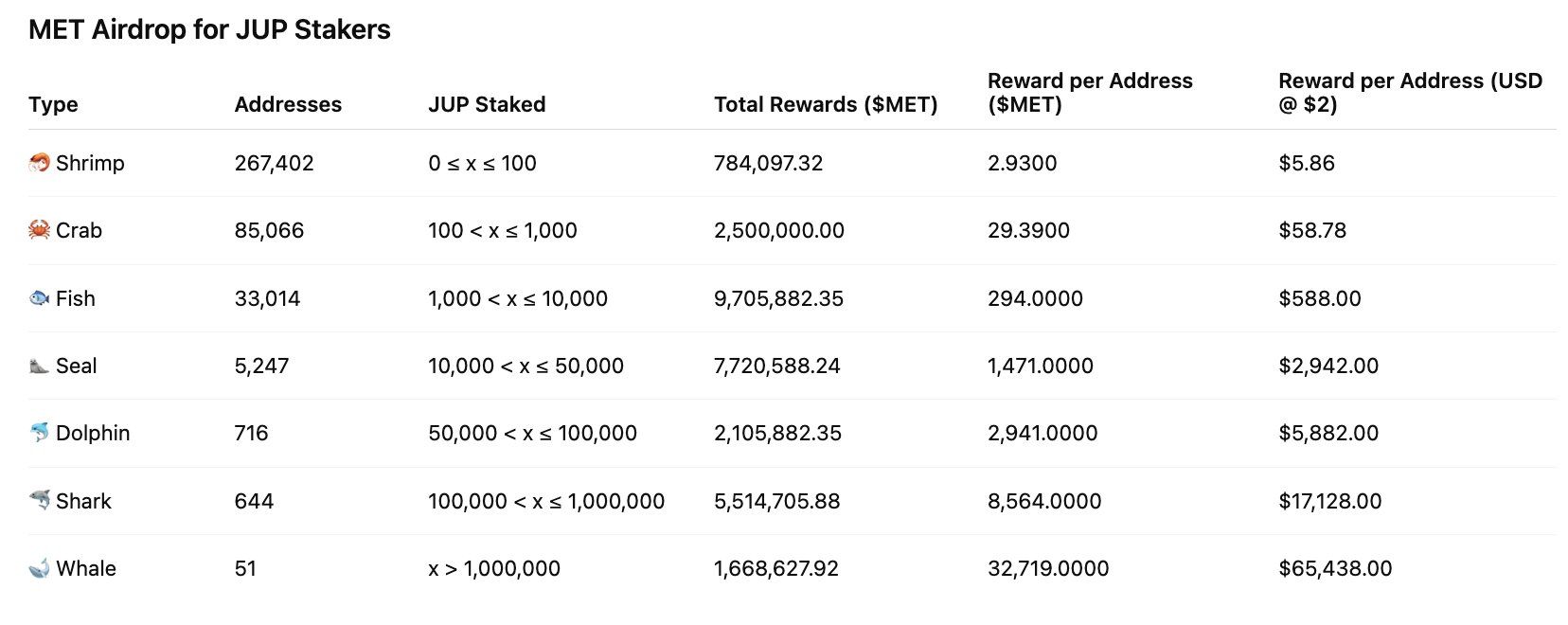

3% Allocation for JUP Staker

As BeInCrypto reported, Meteora is getting ready for a TGE in October. The platform floated one of many group’s most notable proposals forward of MET’s TGE.

Sponsored

Sponsored

Under the plan, the venture intends to allocate 3% of the TGE fund to Jupiter’s JUP stakers as Liquidity Position NFTs. Specifically, Meteora would use the three% to seed MET liquidity in a Single-Sided DAMM V2 pool, then allocate positions to Jupiter stakers based mostly on time-weighted staking, quantity, and voting exercise.

The goal is to create MET/USDC liquidity at itemizing with out instantly including extra MET to the circulating provide. The proposal additionally emphasizes that “no additional tokens circulating will be added due to this proposal.” This is a “liquidity-first” method slightly than a direct token payout.

Meteora’s Co-Lead, Soju, printed a public calculation to visualize scale. According to Soju, roughly 600 million JUP are at present staked. A 3% allocation would equal 30 million MET tokens. That works out to about 0.05 MET per staked JUP.

“I think its reasonable,” Soju shared.

A consumer on X ran some serviette math and produced an identical determine of ~0.05035 MET/JUP relying on FDV assumptions. The per-JUP reward is small however aggregated at scale, so it might probably function a significant incentive to convert customers into MET liquidity suppliers.

Pros & Cons

Meteora’s proposal has clear upsides in contrast to different tasks that reward customers via airdrops. It explicitly acknowledges Jupiter’s function within the Solana ecosystem, helps bootstrap MET/USDC liquidity at TGE, and reduces the speedy promote strain as a result of the preliminary reward is a liquidity place slightly than freely tradable tokens. With cautious engineering (time-weighted distribution, vesting connected to NFTs, withdrawal restrictions), this could possibly be an efficient bridge between the 2 communities.

However, important dangers stay. The group has raised equity considerations: why should JUP stakers receive a large share? Could an “LP Army” or giant wallets seize a disproportionate share of the rewards? What will the circulating provide be at TGE instantly? Earlier allocation drafts talked about up to 25% reserved for liquidity/TGE reserve, so the full preliminary circulating provide stays a fabric transparency query.

“Difficult to debate on ‘fairness’ when JUP gave up 5% for Meteora (via mercurial stakeholders). LP army deserves more -> LP Army will capture a significant chunk of all future emissions (ongoing LM rewards), and still possess 20% (8% + 5% + 2% + 3% + 2%) of total supply at TGE,” Soju noted.

From previous airdrop occasions, Meteora’s workforce should be clear about tokenomics, clearly disclose the LP NFT redeem/vest mechanics, set per-address caps, and take into account extra incentives for MET holders. If executed poorly, concentrated distribution and subsequent promote strain might erode TGE’s worth.

{kind=link}