In a notice printed on Tuesday, Jurrien Timmer, Director of Global Macro at Fidelity Investments, discusses how a shifting financial panorama might affect markets, central financial institution coverage, and the trajectory of each Bitcoin and gold. With the S&P 500 hitting new highs and the so-called “Trump Trade” reversing course, Timmer gives nuanced insights into fiscal coverage, inflation, and the position of threat property in a “limbo” market setting.

The Trump Effect

Timmer observes that the primary six weeks of 2025 have introduced surprising market strikes and an unusually excessive “noise-to-signal ratio.” The dominant market expectation coming into the yr—anticipating “higher yields, a stronger dollar, and outperforming US equities”—has abruptly flipped. He notes: “It seems so 2025 that the consensus trade of higher yields, a stronger dollar, and outperforming US equities has turned into the opposite.”

Timmer highlights that Bitcoin, contemporary off a year-end rally, stays on prime of rolling three-month return rankings, adopted carefully by gold, Chinese equities, commodities, and European markets. At the decrease finish of the desk, the US greenback and Treasuries are citing the rear.

Related Reading

Despite the S&P 500’s report ranges, Timmer calls this a “digestion period” following the post-election optimism. He explains that the market beneath the headline index is far much less decisive. According to Timmer, the equal-weighted index stays on maintain, with solely 55% of shares buying and selling above their 50-day shifting averages.

“Sentiment is bullish, credit spreads are narrow, the equity risk premium (ERP) is in the 10th decile, and the VIX is at 15. The market appears to be priced for success.” Timmer underscores that whereas earnings development was sturdy at 11% in 2024, revisions seem lackluster, and there are open questions on what may occur if long-term charges climb in the direction of 5% or past.

One of essentially the most essential items of Timmer’s evaluation facilities on Federal Reserve coverage. He factors to the current CPI report, with a year-over-year core inflation determine of three.5%, as a near-consensus indicator that the Fed will stay on pause. “It’s now all but unanimous that the Fed is on hold for some time to come. That’s exactly right, in my view. If neutral is 4%, I believe the Fed should be a smidge above that level, given the potential likelihood that ‘3 is the new 2.’”

He warns about the opportunity of a “premature pivot,” recalling the coverage errors from the 1966–1968 interval, when charge cuts occurred too early, finally permitting inflation to achieve a foothold.

With the Fed apparently sidelined, Timmer believes the following market driver for rates of interest will come from the lengthy finish of the curve. Specifically, he sees pressure between two eventualities: one that includes infinite deficit spending and rising time period premiums—hitting fairness valuations—and one other emphasizing fiscal self-discipline, which might presumably rein in long-dated bond yields.

Timmer additionally remarks that weekly jobless claims might come into sharper focus for bond markets, given how authorities spending below the brand new administration might affect employment information.

Related Reading

Timmer factors out a possible bullish sample—a head-and-shoulders backside—within the Bloomberg Commodity Spot Index. Though he stops in need of calling it a definitive shift, he notes that commodities stay in a broader secular uptrend and will see renewed investor curiosity if inflation pressures keep elevated or fiscal circumstances stay free.

Gold, he notes, has been “a big winner” lately, outperforming many skeptics’ expectations: “Since 2020, gold has produced almost the same return as the S&P 500 while having a lower volatility. In my view, gold remains an essential component of a diversified portfolio in a regime in which bonds might remain impaired.”

Timmer sees gold testing the essential $3,000 stage amid a worldwide uptick in cash provide and a decline in actual yields. Historically, gold has proven a robust detrimental correlation with actual yields, although Timmer believes the steel’s power of late may additionally replicate fiscal slightly than financial dynamics—notably, geopolitical demand from central banks in China and Russia.

Bitcoin Vs. Gold

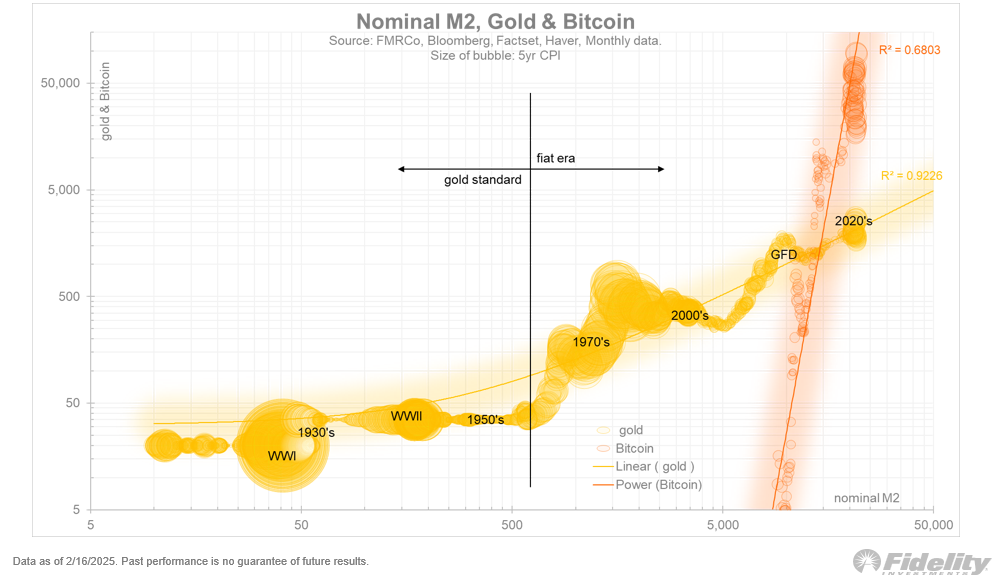

According to Timmer, the outperformance of each gold and Bitcoin has “sparked a lot of conversation about monetary inflation.” However, he attracts a distinction between the “quantity of money” (the cash provide) and the “price of money” (value inflation).

“The point of this exercise is to show that the growth in traditional asset prices over time can’t just be explained away by monetary debasement (which is a favorite pastime of some bitcoiners),” he writes.

Timmer’s charts recommend that whereas nominal M2 and nominal GDP have moved in close to lockstep for over a century, shopper value inflation (CPI) has lagged considerably behind cash provide development. He cautions that adjusting asset costs solely in opposition to M2 might produce deceptive conclusions.

Still, his evaluation finds that each Bitcoin and gold have strong correlations to M2, albeit in numerous methods: “It’s interesting that there’s a linear correlation between M2 and gold, but a power curve between M2 and Bitcoin. Different players on the same team.”

Timmer highlights gold’s long-run efficiency since 1970, noting that it has successfully saved tempo—and even exceeded—the worth created by many bond portfolios. He sees gold’s position as a “hedge against bonds,” particularly if sovereign debt markets stay pressured by fiscal deficits and better long-term charges.

Timmer’s notice underscores that Bitcoin’s robust efficiency can’t be seen in isolation from gold or the broader macroeconomic setting. With yields in flux and policymakers grappling with deficits, buyers could also be compelled to reassess the traditional 60/40 portfolio mannequin.

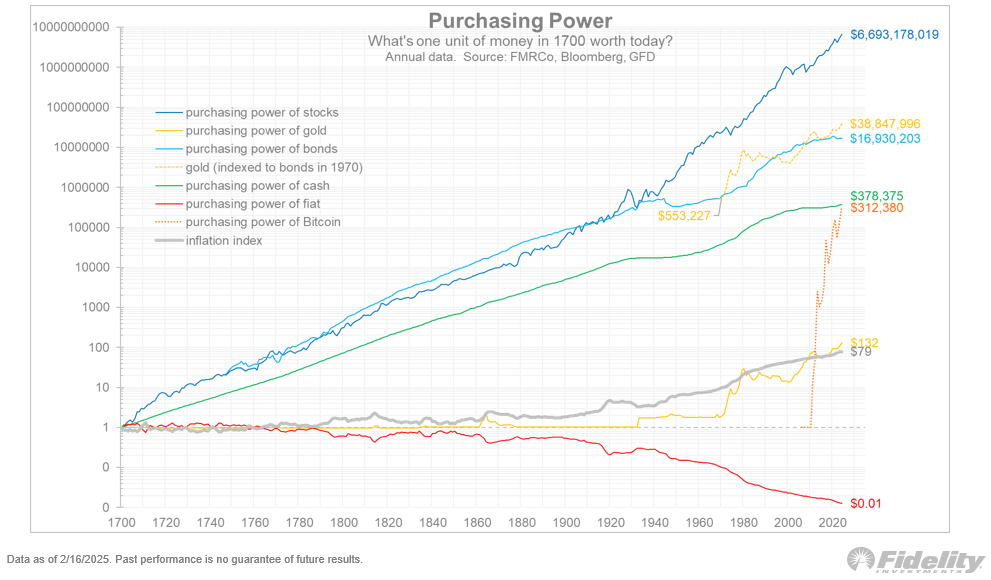

He emphasizes that whereas previous expansions of the cash provide have usually spurred inflation, the connection shouldn’t be all the time one-to-one. Bitcoin’s meteoric rise might, in Timmer’s view, replicate a market notion that fiscal issues—not simply financial coverage—are driving asset costs. “And as you can see from the dotted orange line and the green line, Bitcoin has added the same amount of value that overnight money took over 300 years to create,” he concluded.

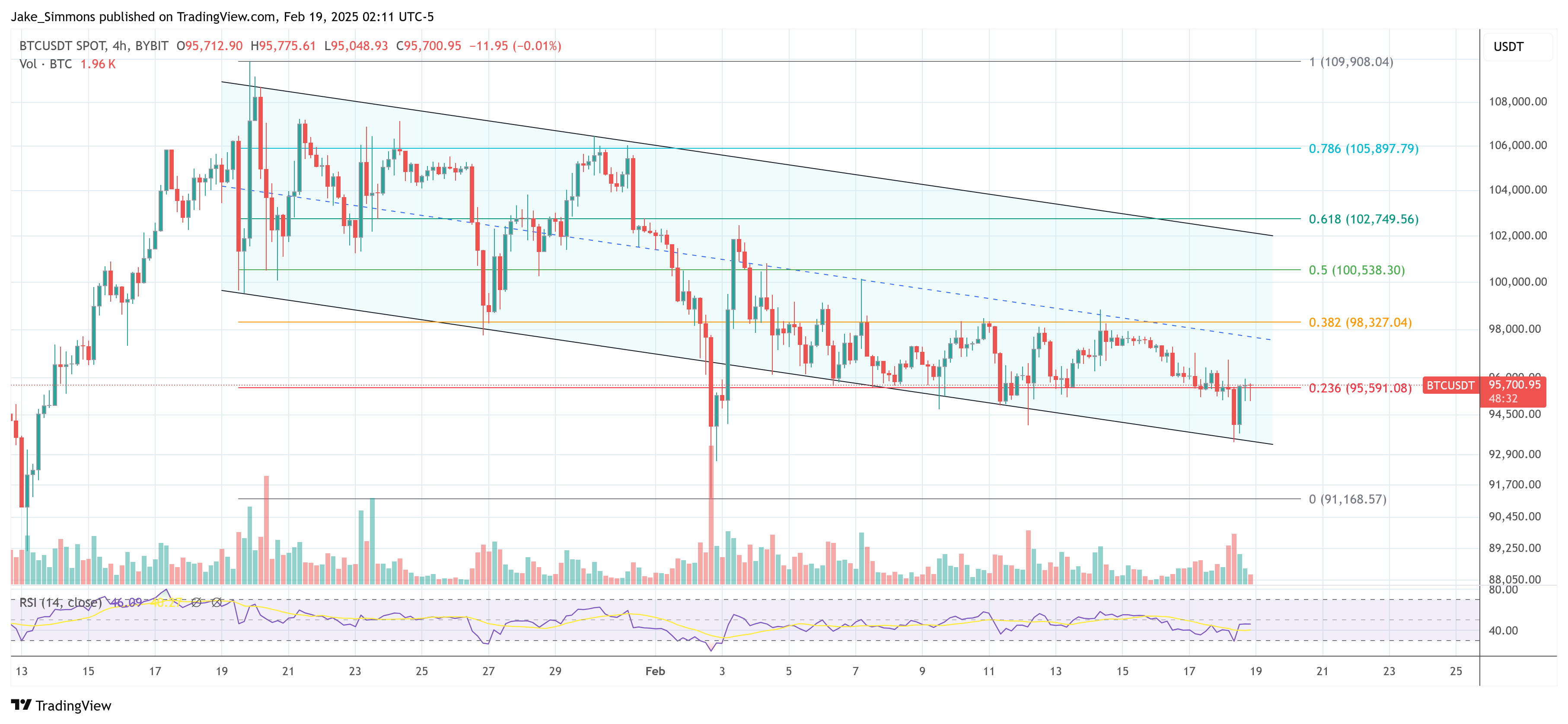

At press time, BTC traded at $95,700.

Featured picture from YouTube, chart from TradingView.com

{kind=link}